Explore 和 Exploit 是做推荐的常用问题,由于推荐的点击率/转化率模型是由历史数据产生的,对新的item点击率估计误差会很大,需要对曝光不足的item进行探索。

考虑多臂老虎机问题,即有N个老虎机,每个臂有概率 Pi 会有奖励,并且这个概率不随时间变化。

显然,最优策略是选择概率 Pi 最大的那个臂不停地摇,每次期望回报最大 $(r^* = \max_i p_i)$,

而由于一开始不知道 Pi ,所以实际第t步的回报期望可能小于最大值。定义 $(r_t)$为第t步的回报,如果有奖励,回报为1,否则回报为0.

其期望值等于摇的那个臂对应的 Pi 的值。

可以定义 regret 为他们的差 $(regret_t = r^* - E r_t)$。

## 多臂老虎机仿真 import numpy as np n = 10 # 10个臂 bandit_p = np.random.rand(n) def gen_data(i): assert i < n if np.random.rand() < bandit_p[i]: return 1.0 # reward return 0.0 # no reward

在这个问题中,一般有这些经典的探索方法:

- 随机策略:随机选择一个动作,简称瞎猜,每一个动作都有概率。所以 $( regret = \max_i p_i - \bar{p_i} )$

def random_select(ctx): return np.random.randint(ctx['n'])

- 确定性策略:每次都选择当前最优的动作,如果最优动作很多个,随机选一个

# 稍作修改,前n次依次选择每一个动作 def determine_select(ctx): if ctx['step'] < n: return ctx['step'] return np.argmax(ctx['cum_reward_action'] / (ctx['cum_action']))

- $(\epsilon)$-贪心策略:即以 $(\epsilon)$ 的概率选择随机策略,以 $(1 - \epsilon)$选择确定性策略, $(\epsilon)$ 随着时间衰减

def epsilon_greedy(ctx): epsilon = 1 / (1 + np.sqrt(ctx['step'])) if np.random.rand() < epsilon: # random return random_select(ctx) else: return determine_select(ctx)

- naive 策略: 前N步随机探索, 从第 N+1 步开始,采用确定性策略

def naive_select(ctx): if ctx['step'] < 500: return random_select(ctx) else: return determine_select(ctx)

- softmax 随机策略:即对每一个动作的累积平均回报做softmax归一化,作为每个动作的选择概率

def softmax_select(ctx, n0 = 0.1): if ctx['step'] < n: return ctx['step'] avg_reward = ctx['cum_reward_action'] / (ctx['cum_action']) p = np.exp(avg_reward / n0 ) p = p / np.sum(p) return np.random.multinomial(1, p)[0]

- thompson 采样: 认为每个动作的Pi 服从Beta(a, b)先验分布, 而每个动作的历史平均回报后验分布则服从 Beta(a + win, b + loss) 分布,确定性策略相当于按照后验分布的均值/众数 选择最优策略,然而前期由于探索不充分,这种估计方差很大,必然要引入随机性进行探索,Thompson的方法是从后验分布中采样一个值代替对Pi的估计,然后按照确定性策略选择动作。

def thompson_select(ctx): win = ctx['cum_reward_action'] loss = ctx['cum_action'] - win p = np.zeros(n) for i in range(n): # 期望概率 p_i = (1 + win[i]) / (1 + trials[i]), 现在不是用期望的概率,而是引入一定的随机性,随机从p_i服从的后验beta分布中采样一个结果 p[i] = np.random.beta(1 + win[i], 1 + loss[i]) return np.argmax(p)

- UCB方法: 因为利用历史平均回报对Pi估计不准,所以可以用估计的置信区间的上界 $(\bar{r_i} + \sqrt{\frac{2 ln T}{n_i}})$ 作为对Pi的乐观估计。

然后采用确定性策略。其中 T 是总的步数, n_i 是第i个臂被选择的次数。

def ucb_select(ctx): if ctx['step'] < n: return ctx['step'] cum_n = ctx['step'] + 1.0 up_bound = ctx['cum_reward_action'] / (ctx['cum_action']) + np.sqrt(1.0 * np.log(cum_n) / ctx['cum_action']) return np.argmax(up_bound)

- 仿真代码

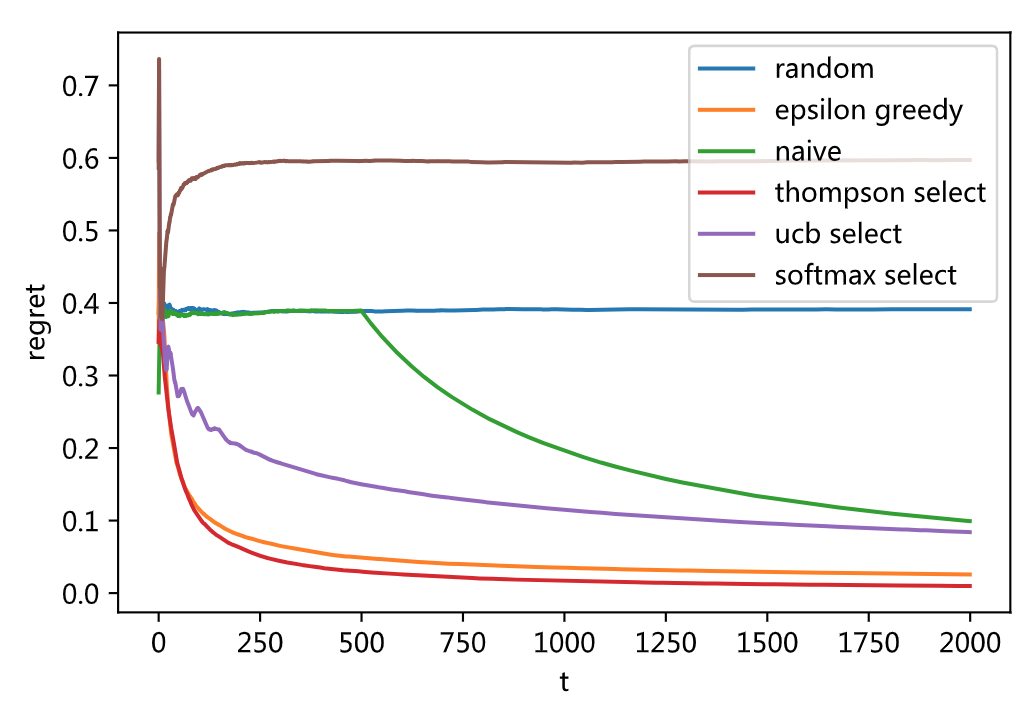

import matplotlib.pyplot as plt from numba import jit import logging @jit def simulation(select_action, n_ = 3000): t = [] reward = [] cum_reward_per = 0.0 cum_reward_action = np.zeros(n) cum_action = np.zeros(n) for i in range(n_): t.append(i) ctx = {'n' : n, 'cum_reward_action' : cum_reward_action, 'cum_action' : cum_action, 'step': i} action = select_action(ctx) cum_action[action] += 1 r = gen_data(action) action_n = cum_action[action] cum_reward_action[action] += r cum_reward_per += r reward.append(cum_reward_per) return np.array(t), np.array(reward) @jit def run(select_action, rnd_ = 100, n_ = 3000): t = [] avg_reward = 0 for i in range(rnd_): t, reward = simulation(select_action, n_) avg_reward = avg_reward * i / (i + 1) + reward / (i+1) logging.info("simulate %d round." % (i)) return t, np.max(bandit_p) - avg_reward /(1 + np.arange(n_)) def main(): n_ = 2000 t, r = run(random_select, n_ = n_) plt.plot(t, r) t, r = run(epsilon_greedy, n_ = n_) plt.plot(t, r) t, r = run(naive_select, n_ = n_) plt.plot(t, r) t, r = run(thompson_select, n_ = n_) plt.plot(t, r) t, r = run(ucb_select, n_ = n_) plt.plot(t, r) t, r = run(softmax_select, n_ = n_) plt.plot(t, r) plt.legend(['random', 'epsilon greedy', 'naive', 'thompson select', 'ucb select', 'softmax select']) plt.xlabel('t') plt.ylabel('regret') plt.show() if __name__ == '__main__': main()